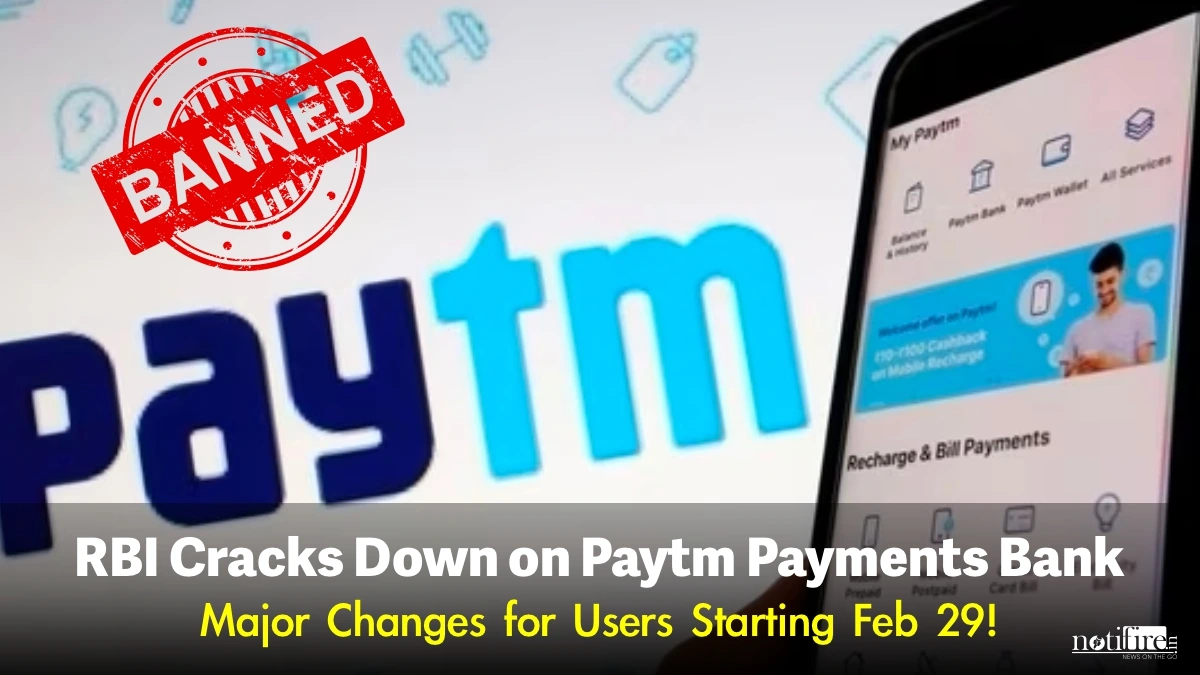

Breaking: RBI Cracks Down on Paytm Payments Bank – Major Changes for Users Starting Feb 29!

July 1, 2024

New - Delhi

The Reserve Bank of India (RBI) has recently imposed a set of significant restrictions on Paytm Payments Bank, a move that has stirred the Indian banking and fintech sector. Effective February 29, these new regulations are set to change how both new and existing customers interact with Paytms banking services. This article breaks down the situation into five key points, offering a clear understanding of the impact on users and the companys response.

The RBIs decision comes after an audit report highlighted persistent non-compliance and continued material supervisory concerns with Paytm Payments Bank. Established in 2017, Paytm Payments Bank (PPBL) has been a digital banking pioneer in India. However, the recent findings have led to stringent measures from the central bank, underlining the seriousness of compliance in the fintech sector.

Paytm Share Price Today Live Updates

One of the immediate effects of RBIs decision is the stoppage of new customer onboarding after February 29. This means potential Paytm users looking to set up new accounts will be unable to do so. The restriction is a significant setback for Paytm, which has been aggressively expanding its user base.

Existing Paytm users will face limitations too. Post-February 29, they will not be able to use their Paytm wallets, Paytm Fastags, or Mobility Cards for transactions. This restriction considerably reduces the utility of Paytms digital wallet and associated services, impacting a large portion of its customer base.

In response to the RBIs restrictions, Paytm Payments Bank Limited has stated that it is taking immediate steps to comply with the RBIs directions. The bank is working closely with the RBI to address their concerns as swiftly as possible.

One97 Communications Limited (OCL), the parent company of Paytm, has announced that it will now work exclusively with other banks, distancing itself from Paytm Payments Bank for certain operations. This strategic shift indicates Paytms agility in adapting to regulatory challenges and its commitment to continue providing financial services.

Customers should be aware that after February 29, they will neither be able to receive nor send money from their Paytm accounts. However, they are allowed to withdraw the existing balance. This limitation not only affects direct transactions but also services like fund transfers, bill payments, and UPI facilities through Paytm.

The restrictions primarily target Paytms banking operations, suggesting that transactions made via external banks might not be affected. Customers may still use Paytm for digital payments if their account is linked to an external bank, though the usability of Paytm Wallet remains uncertain.

Despite the restrictions, Paytm assures that its other financial services, including loan and insurance distribution, are unaffected. These services operate independently of the Paytm Payments Bank and will continue as usual.

The RBI has also mandated the termination of all nodal accounts of One97 Communications Ltd and Paytm Payments Services Ltd. This move ensures that payments collected from customers are released to vendors without delays, emphasizing the importance of financial discipline in digital transactions.

The RBIs actions signify a pivotal moment for the digital banking sector in India, highlighting the criticality of regulatory compliance. For Paytm, this is a time of strategic realignment and adaptation. For customers, its a period of transition and understanding the new dynamics of digital transactions.

As we await further clarifications and developments, the situation underscores the evolving nature of fintech and the need for both providers and users to remain agile and informed. Paytms journey, amid these challenges, will be closely watched as a barometer for the health and direction of digital banking in India.

Read

Subscribe to our newsletter and never miss a story

Read

Read

Subscribe to our newsletter and never miss a story

Comments: 0